In October 2022, the installed battery capacity turned negative month-on-month, and the market share

In October 2022, the installed battery capacity turned negative month-on-month, and the market share of Ningwang this year is likely to be less than 50%

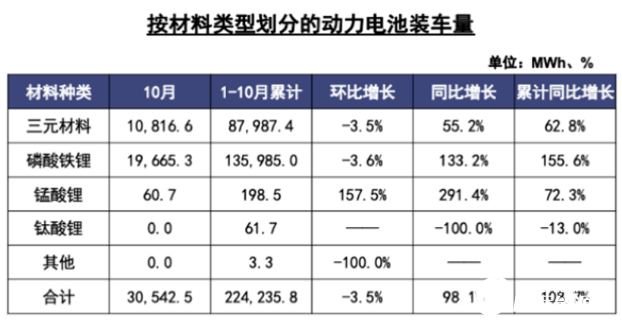

This year, the "gold, silver and ten" in the auto market failed to arrive as scheduled. Especially in October, there was a significant gap between the sales volume of new energy vehicles and the month-on-month level in previous years (about 150% year-on-year in previous years, and more than 5% month-on-month). In October this year, the sales volume dropped to double digits 85.8% year-on-year and only 0.4% month-on-month). This also led to a certain degree of correction in the output and installed volume of power batteries in October from the same month-on-month growth level. In October, the output of power batteries reached 62.8GWh, with a year-on-year growth of 150.1% and a month-on-month growth of 6.2%. The installed capacity reached 30.5GWh, up 98.1% year on year and down 3.5% month on month.

As for lithium iron phosphate batteries and ternary lithium batteries, the output of ternary lithium batteries in October this year was 24.2GWh, up 163.5% year on year, accounting for 38.6%, down 0.2% month on month. The installed capacity was 10.8GWh, accounting for 35.4%, up 55.2% year on year and down 3.5% month on month. The production of lithium iron phosphate battery was 38.6GWh, with a year-on-year increase of 142.6%, accounting for 61.4%, and a quarter-on-quarter increase of 10.8%. The installed capacity was 19.7GWh, maintaining a year-on-year growth of 133.2%, accounting for 64.4%, and a month-on-month decline of 3.6%.

1. Lithium iron phosphate battery is still dominant in output, installed capacity and export

As shown above, near the end of the year, lithium iron phosphate battery still occupies a dominant position in the output and installed volume, which is not only reflected in the specific proportion, but also in the respective year-on-year growth rate. The quarter-on-quarter growth rate is affected by the decrease in terminal sales volume, and the dominant trend of lithium iron phosphate battery is more obvious when deduced to the terminal.

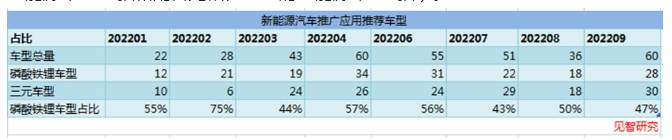

According to the ninth batch of Recommended Models Catalogue for New Energy Vehicle Promotion and Application recently released by the Ministry of Industry and Information Technology, there are up to 28 new energy models equipped with lithium iron phosphate batteries in new energy passenger vehicles (in addition, there are 30 new energy models equipped with three-way batteries and 2 new energy models equipped with cobalt-free lithium batteries).

And the annual promotion of new energy passenger vehicles in the proportion of lithium iron phosphate battery equipped with more than 52%, compared with the previous two years in 2020 and 2021 new energy vehicle promotion and application recommended model catalog of 15% and 42% lithium iron phosphate battery equipped level, this year the proportion of lithium iron phosphate battery is expected to be more than three yuan lithium battery, and continue to maintain next year.

And it is worth mentioning that, in addition to the domestic car enterprises for the high level of lithium iron phosphate battery favor steadily maintained, the proportion of overseas lithium iron phosphate battery has also significantly increased, before the overseas new energy vehicle enterprises choose to support the three-way lithium battery on the car, but from this year's power battery export level lithium iron phosphate battery is superior, The main reason is that the production capacity of lithium iron phosphate battery of overseas power battery manufacturers has not been able to rapidly increase. The main source of lithium iron phosphate battery is still domestic. At the same time, since this year, many overseas new energy vehicle enterprises have launched the model version of lithium iron phosphate battery.

In October, the export volume of power batteries was 14.7GWh, among which the export volume of three-way batteries reached 4.3GWh, while the export volume of lithium iron phosphate batteries was 10.3GWh. Lithium iron phosphate batteries occupy the largest proportion, even more than that of the domestic market, reaching 70%.

2, Ningde Times market share this year for the first time below 50%

Five years ago, when China's power battery supply white list was just released, the number of power battery manufacturers reached more than 200 at its peak, and the top ten power battery manufacturers accounted for less than 20% of the total installed capacity. However, in just five years, the competitive landscape of power battery manufacturers has changed dramatically. As of October this year, the number of power battery manufacturers that can effectively load vehicles has dropped to 40.

While the top three, top five and top ten power battery enterprises in terms of load capacity reach 24.6GWh, 26.6GWh and 29.1GWh respectively, accounting for 80.4%, 87.2% and 95.3% of the total load capacity, respectively. The top 10 power battery makers managed only 4.7% of the market, compared with 8.2% a year earlier.

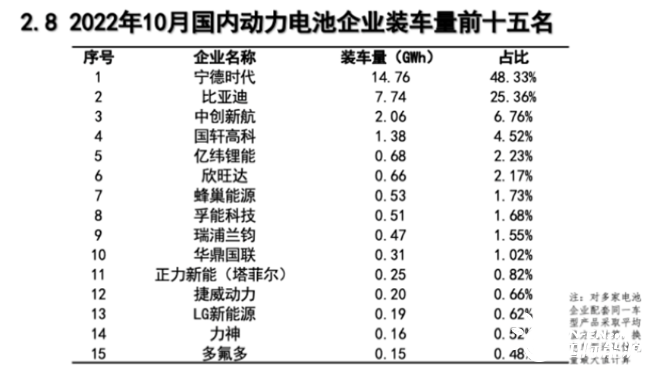

The number of installed power batteries in October was still the champion of Ningde era, with the total installed volume of 14.76GWh, accounting for 48.33% (49.9% in the same period last year), among which the installed volume of terpolymer lithium batteries was 6.75GWH, accounting for 62.42%, and the installed volume of lithium iron phosphate batteries was 8.01GWH, accounting for 40.73%. Considering that the installed capacity of Ningde Times is below 50% in 8 of the previous 10 months, if the installed capacity of Ningde Times does not increase significantly in the following two months, the proportion of the total installed capacity of Ningde Times in China may be below 50% for the first time this year.

The main reasons behind the decline of Ningde Era's installed volume this year are two points:

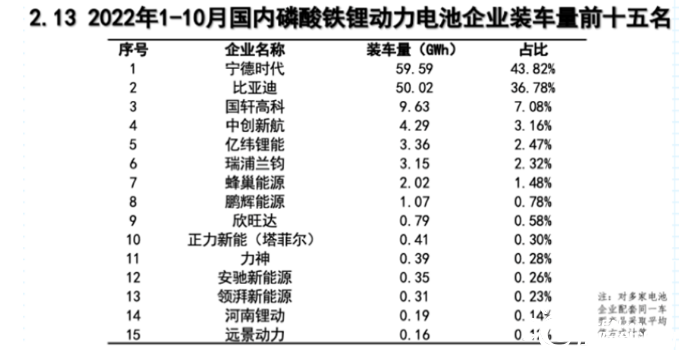

On the one hand, the "second place" in the fields of lithium iron phosphate battery and lithium ternary battery has made considerable progress this year. Among them, the power battery manufacturer Ferdi Battery has benefited from the fact that BYD's car products have not been affected by the epidemic this year, and its monthly sales have been increasing month by month. From January to October this year, BYD's car product market share has exceeded 30%. As a result, the proportion of domestic installed lithium iron phosphate battery continued to increase, from January to October, the proportion of lithium iron phosphate battery installed has reached 36.78%, ranking the second place, and the first place Ningde era gap only 7.04 percentage points, and in April this year also completed the first time to surpass Ningde era to become the first installed lithium iron phosphate battery.

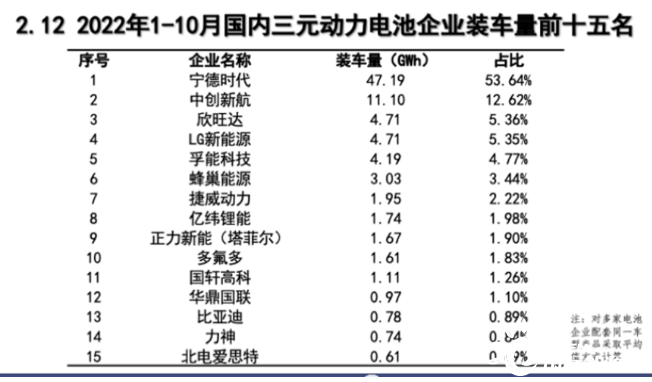

Meanwhile, Zhongchuang Singapore Airlines, which successfully entered GAC Aean's power battery supply chain with a low price strategy and became its main supplier, also benefited from the rapid growth of GAC Aean's sales volume this year (GAC Aean's sales volume increased from around 10,000 units at the beginning of the year to around 30,000 units in October and maintained a stable sales volume, which is expected to replicate BYD's monthly sales growth pattern last year). In addition, the proportion of ternary lithium battery installed level has improved. From January to October, the proportion of ternary lithium battery installed level of Singapore Airlines has reached 12.62%, ranking the second (the previous level of about 8%).

On the other hand, several major customers of NEV enterprises ranked higher than those of the previous year in Ningde Times this year have been affected by the epidemic for many times, leading to difficulties in production, transportation, supply and sales, etc. Tesla, the largest customer of lithium iron phosphate battery of Ningde Times, and some new car makers such as NIO and Ideo have been affected the most. In the first ten months of this year, the market share of Tesla has fallen below 10% to 8.3%, and the sales fluctuations of terminal new energy vehicles directly lead to the continuous decline of the domestic market share of lithium iron phosphate batteries in the Ningde era.

Of course, from the perspective of the global power battery installed level, Ningde Times will also shift more focus to overseas this year. In the first three quarters of this year, the global electric vehicle power battery installed volume was 341.3GWh, a year-on-year growth of 75.2%. The installed volume of Ningde Times was 119.8GWh respectively, with a market share of 35.1%. Compared to the same period last year, the power battery market share increased by about 4 percentage points, which is much faster than the overseas progress of a number of second-tier domestic power battery manufacturers (for example, the global power battery market share of CSIA increased by 1.1 percentage points, and the global power battery market share of Guoxen Advanced Technology increased by 0.9 percentage points).

Source: Wall Street See

;){kind=link}