A car stuck in a power battery

The company specializes in household energy storage, and the analysis shows that automobile companies frequently move in the field of power battery.

The signing ceremony of BMW's new power battery project was held in Shenyang recently. BMW's Shenyang production base will carry out a large-scale expansion of power battery production. The total investment of the project is about 10 billion yuan.

In addition, GAC, Honda, NIO and other car companies are also accelerating the promotion of power battery projects, and even involved in the most upstream lithium mines. Why do car companies repeatedly layout power batteries?

Chang 'an Automobile Chairman Zhu Huarong's words, or visible. At the 12th China Automobile Forum, he bluntly said: "Lack of core, expensive electricity" has led to the loss of 606,000 units of Changan Automobile production capacity this year.

When describing the power battery problem, Zhu Huarong used the term "high power" rather than "lack of power." That is to say, today's new energy vehicle industry, there is no shortage of power battery supply, but the battery is too expensive, the pressure to the downstream car enterprises. Because of this, more and more car companies choose to make their own batteries.

Let the car enterprise "flesh pain" power battery

According to data from Shanghai Steel Union, the price of battery grade lithium carbonate has risen again recently, once approaching 600,000 yuan/ton. In the beginning of 2021, the price of lithium carbonate was still around 50,000 yuan/ton, which increased about 12 times in more than a year.

Upstream prices have soared, squeezing the middle and downstream. The pressure of the power battery enterprises, and transferred the cost pressure to the car enterprises, the car enterprises became the least profitable one. In the third quarter of this year, with the exception of BYD, few car companies saw net profit growth faster than midstream power battery companies and upstream lithium miners.

Before that, there had been a car enterprise boss said "car enterprises in the battery factory to work".

Take NiO as an example. In the third quarter of this year, its gross profit margin on vehicle sales was 16.4%, down 8.9% year-on-year. Li Bin, founder and CEO of NIO, said gross margin was challenged by battery prices this year.

"Lithium carbonate prices hit a new high, battery prices are not in short supply, I think lithium prices should go down. When the unit price of lithium carbonate drops by 100,000 yuan, the gross profit margin will increase by 2%. At present, the unit price of lithium carbonate is about 600,000 yuan. If it can drop to 400,000 yuan, we can increase the gross profit margin by 4 points." He also points out that for mass markets, it is very difficult to achieve 20%-25% gross margins without vertical integration capabilities.

That is why many carmakers are helping their secondary suppliers and making batteries like BYD's to cut costs.

Toward self-production, self-research

On November 11, BMW's new power battery project signing ceremony was held in Shenyang. According to the agreement, BMW Shenyang production base will carry out a large-scale expansion of power battery production. The new power battery project is funded by BMW Brilliance with a total investment of about 10 billion yuan. It is also another major investment after the total investment of 15 billion yuan in the Rida plant.

Regarding the project, BMW told reporters: "The BMW Brilliance Power Battery Center, which opened in 2017, is the BMW Group's first fully equipped battery center outside Germany. After years of development, BMW Shenyang production base has established a strong local electrification capability system integrating supply chain, research and development, power battery and electric vehicle production."

"As the world's largest power battery production base and consumer market, China has formed a huge ecosystem," an industry insider said. "Power batteries are a core component of electric vehicles. BMW's efforts to strengthen research and production of power batteries will help enhance competitiveness and make it easier to control costs."

BMW is expanding its power battery plant because it needs more capacity to carry out its new energy strategy.

BMW delivered a total of about 592,900 BMW and MINI cars to Chinese customers in the first nine months of this year, according to official data. Among them, BMW's pure electric model sales increased 65% year on year.

By 2023, BMW plans to increase its pure electric products in China to 13; By the end of 2025, BMW plans to deliver 2 million pure electric vehicles worldwide; By 2030, at least 50% of BMW's global sales are expected to come from pure electric models.

By 2030, BMW Group's other three brands will also be fully electrified: Rolls-Royce brand will complete the electrification of all products; BMW Motorrad urban mobility series will be fully electric; The MINI brand will also go fully electric from the early 2030s.

In order to achieve this plan, in addition to the expansion of battery production, BMW Group also awarded Ningde Times and Yi Wei Lithium Energy cell production contracts worth more than 10 billion euros. The two companies will build cell plants in China and Europe, each with an annual capacity of 20GWh.

BMW is not alone in beefing up its batteries. On November 15, South Korean media reported that Samsung SDI is accelerating the establishment of a joint venture battery plant with General Motors and Volvo.

Samsung and General Motors plan to build a plant with an annual capacity of 50GWh to meet the demand for batteries to power 670,000 electric vehicles with a range of 500km, the report said. Samsung SDI and GM will invest about $2 billion each.

In addition, Samsung SDI is pushing for a separate joint venture with Volvo, which South Korean media say will be announced in December. The joint venture will be similar in size to the Samsung-GM joint venture, and the two companies will each invest about $2 billion in the joint venture plant, which will produce 50GWh of batteries per year, according to the company.

Domestic car companies are also increasing their size. On October 27, GAC Aean announced the establishment of Inpai Battery Technology Co., LTD., which is jointly invested by GAC Aean, GAC Passenger Car and GAC Commerce and controlled by GAC Aean. Located in Panyu District, Guangzhou City, the company has a total investment of 10.9 billion yuan to carry out the industrialization construction of battery self-research and production, as well as the production and sales of independent batteries.

So far, GAC Group's layout picture in the battery field is presented one by one: it has a joint venture with Ningde Times, invests in Qingtao, invests in Xinhang, joins hands with Ganfeng Lithium, Shixi Coal industry and Zunyi Energy to get involved in mining, etc. Finally, it develops its own cell and builds its own cell factory.

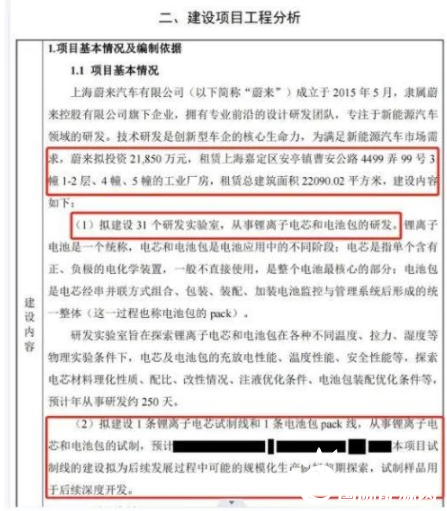

Nio Battery project document.

New car manufacturers are not to be outdone. On May 23, the Shanghai Environmental Information Disclosure Platform for enterprises and public institutions publicized a new research and development project of NIO, including 31 research and development laboratories engaged in the research and development of lithium-ion cells and battery packs, as well as a lithium-ion cell trial production line and a battery pack line. The project is expected to be constructed between August and October this year with an investment of 218.5 million yuan. Judging from the EIA report, this high probability is just a test of the water project. But this research and development project has covered the whole process from raw materials to cell production to inspection and testing.

In the second quarter analysis meeting, Li Bin disclosed the layout of NIO in the battery field for the first time. Nio has set up a battery research and development team of more than 400 people, and is deeply involved in the research and development of battery materials, cell and package design, battery management system, manufacturing process, etc., to comprehensively establish and enhance the battery systematic research and development and industrialization capabilities.

He revealed that the mass production of the self-developed battery is expected to be in the second half of 2024, in the price range of 200,000 to 300,000 yuan NexteV new brand models. Reporters on November 15 to NIO for consultation on the latest progress of battery layout, did not get more information.

Nio's "ambition" also extends to the upstream of the industrial chain. On Sept 25, NIO's wholly-owned subsidiary Blue Northstar Limited entered into a strategic financing deal with Australian mineral exploration and development company Greenwing Resources Limited, which plans to invest more than 100 million yuan in Greenwing to advance its exploration plans for the lithium project in SAN Jorge Salt Lake in Catamarca province, Argentina.

When "Short term" meets "Long Term"

Battery is one of the most important parts of new energy vehicles, accounting for about 40 or 50 percent of the production cost. Battery performance and brand have become important decision-making factors for consumers to buy a car.

Byd has already made a name for itself in new-energy vehicles. Byd has been making big strides in power batteries since the introduction of blade batteries. In 2020, BYD's market share of power battery installations was 14.9%, but in the first 10 months of 2022, BYD's market share of power battery installations has reached 22.66%.

In the power battery circuit, BYD is struggling to catch up with Ningde era this big brother, the gap between the two sides gradually narrowed. In addition, BYD's power batteries also began to supply the road, many car companies are in talks to cooperate.

Seeing BYD's success, many auto companies have planned a route for their own batteries: self-research, self-production and self-supply, reduce battery costs, and even build brands to supply other enterprises, forming a new growth point. But the past experience shows that self-study is not an easy road.

In 2007, Nissan and NEC jointly established AESC to supply batteries for the Nissan Leaf, the world's first mass-commercialized pure electric vehicle. At the time, the power battery industry was still in its infancy, and Nissan's move to develop its own battery was not unusual.

AESC is headquartered in Kanagawa Prefecture, Japan, and began mass production at its first battery plant in 2009, followed by two more in Tennessee and Sunderland in 2012. In 2014, AESC was already the world's second largest producer of electric vehicle batteries, behind Panasonic, with a 21% market share.

In 2015, the Nissan Leaf became the only car in the world to sell more than 200,000 units worldwide, while Tesla's Model S sold fewer than 100,000 units. Judging by these numbers, AESC is also the industry leader.

All looks well, but in 2016 Nissan decided to sell its 51% stake in AESC, preferring an outside supplier. AESC was eventually acquired by China Vision Group.

In November 2016, then-Chairman Carlos Ghosn explained that being tied to in-house battery production left Nissan without the flexibility to buy cheap third-party batteries. In other words, AESC does not reduce its cost.

Why do batteries made by different carmakers have different outcomes? Longzhong information lithium battery Department manager Luo Xiaoli told reporters that there are two main factors:

First of all, the global power battery market has entered a relatively stable development pattern, Ningde Times, together with the second tier of LG, BYD, Panasonic, leaving other battery manufacturers with a small market share. To get a battery into production against this backdrop, you need to sell enough to spread the cost of research and development.

Secondly, we should look at the control ability of raw materials. With the price of battery grade lithium carbonate rising further, which has reached a high of 600,000 yuan/ton recently, even the profit margin of power battery enterprises has been reduced. It can be said that the price of raw materials has a greater impact on the automobile enterprises whether the battery is produced by itself. Therefore, some automobile enterprises will further layout to the upstream of the industrial chain and cooperate with lithium mining enterprises.

Luo Xiaoli has a positive attitude toward car companies' research and development of power batteries. "In the short term, R&D costs may be raised, but in the long term, if automakers can carry out the layout of the whole industry chain, it will form a closed loop, effectively improve the ability to resist risks and reduce costs. "Just like the development of core components such as engines in the era of fuel cars, the deployment of power batteries is an investment in the future and will be a trend."

Luo Xiaoli also pointed out that, "At present, power batteries are in short supply. In order to reduce supply chain risks, many automobile enterprises choose to expand suppliers. If they can develop and produce their own batteries, they can also be used as bargaining chips to reduce procurement costs, even if they cannot reduce costs and improve efficiency in a short time."

Source: Time Finance APP Author: Zhang Xu

使用微信掃一掃"});){kind=link}