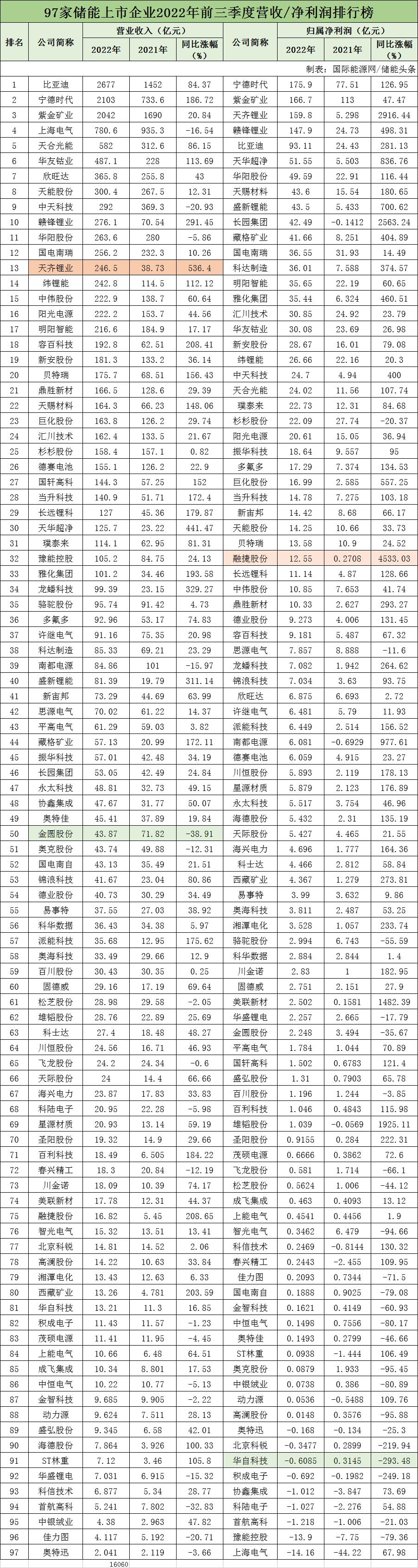

The performance list of 97 energy storage enterprises! Who is the profit king?

At present, Liu Yafang, deputy director of the Science and Technology Department of the Energy Administration, explained in detail that it is estimated that by the end of 2025, the installed operation scale of new energy storage in the power system will reach more than 300 billion kW, with an annual growth rate of more than 50%. In this environment, the performance of listed companies with a reasonable layout of the upstream and downstream industry chain of energy storage is rising.

?Home energy storage, outdoor energy storage, industrial and commercial energy storage in the current market demand exceeds supply.?

Recently, the financial data of listed energy storage companies in the third quarter of 2022 have been released one after another. Disassemble and analyze the financial information of 97 listed energy storage companies from the aspects of operating income, profit, net interest rate, profit rate and debt ratio.

In terms of revenue, BYD topped the list with 267.7 billion yuan, followed by Ningde Times and Zijin Mining. In terms of attributable net profit, Ningde Times ranked first in the first three quarters of 2022 with a net profit of 17.59 billion yuan; The top three on the gross profit margin list are Xizang Mining, Tianqi Lithium and Zangge Mining; From the net interest rate list, Tianqi Lithium has the highest net interest rate, reaching 79.34%; In terms of asset-liability ratio, the debt ratio of Kelu Electronics and ST Lin Heavy is maintained at a high level, and the financial pressure is very big. Byd, Ningde times focus on product research and development, research and development expenses in the top two.

Seventy-nine companies reported higher revenues than a year earlier, while only nine reported losses

In the first three quarters, 97 A-share listed companies participating in the upstream and downstream of the energy storage industry realized A total operating revenue of 1,606 billion yuan and a total net profit attributable to shareholders of listed companies of 1,668 yuan. One hundred million yuan. Of those, 18 reported lower revenue than a year earlier, while nine reported losses.

It has been noted that the growth of many enterprises in the energy storage sector has exceeded market expectations, with shipments saturated and products in short supply. Not only lithium companies with similar production processes have begun to expand the productivity of energy storage business, but also inverter manufacturers have frequently made efforts in the field of energy storage to improve performance growth.

In terms of revenue, there are 33 listed energy storage companies with operating revenue exceeding 10 billion yuan, among which BYD, Ningde Times and Zijin Mining have revenue exceeding 200 billion yuan. In terms of net profit, there are 6 wind power enterprises with net profit of more than 5 billion yuan, of which 4 enterprises - Ningde Times, Zijin Mining, Tianqi Lithium and Ganfeng Lithium - have revenue of more than 10 billion yuan.

In terms of growth, Tianqi Lithium's operating income increased by 580.19% in the third quarter, making it the company with the largest increase in revenue. For the substantial growth, Tianqi Lithium said that the sales volume and the average price of the company's main lithium products increased compared with the same period last year; SES was listed on the New York Stock Exchange, and the passive dilution of SES shares held by the company caused the company no longer to have a significant impact on it. Therefore, it was terminated as a long-term equity investment and recognized as a financial asset measured at fair value and whose changes were included in other comprehensive income, and the investment income was recognized. Combined with SQM's disclosed results in the first half of the year and Bloomberg's forecast of SQM's results in the third quarter, SQM's results from the beginning of the year to the end of the current report are expected to increase significantly compared to the same period last year, resulting in the Company's recognized investment income in the associated Company in the current period increasing significantly compared to the same period last year.

Rongjie shares became 97 listed companies the largest increase in the enterprise. According to the third quarter report of Rongjie in 2022, the net profit of the first three quarters was 1.255 billion yuan, with a year-on-year increase of more than 45 times. The company previously disclosed the third quarter forecast that during the reporting period, the net profit of the parent increased significantly compared with the same period last year, which was caused by the continuous improvement of the new energy industry boom, the continuous increase of the upstream material product demand and price of the lithium battery industry, and the substantial increase of the operating income and profit of the company's lithium concentrate, lithium salt and lithium electrical equipment.

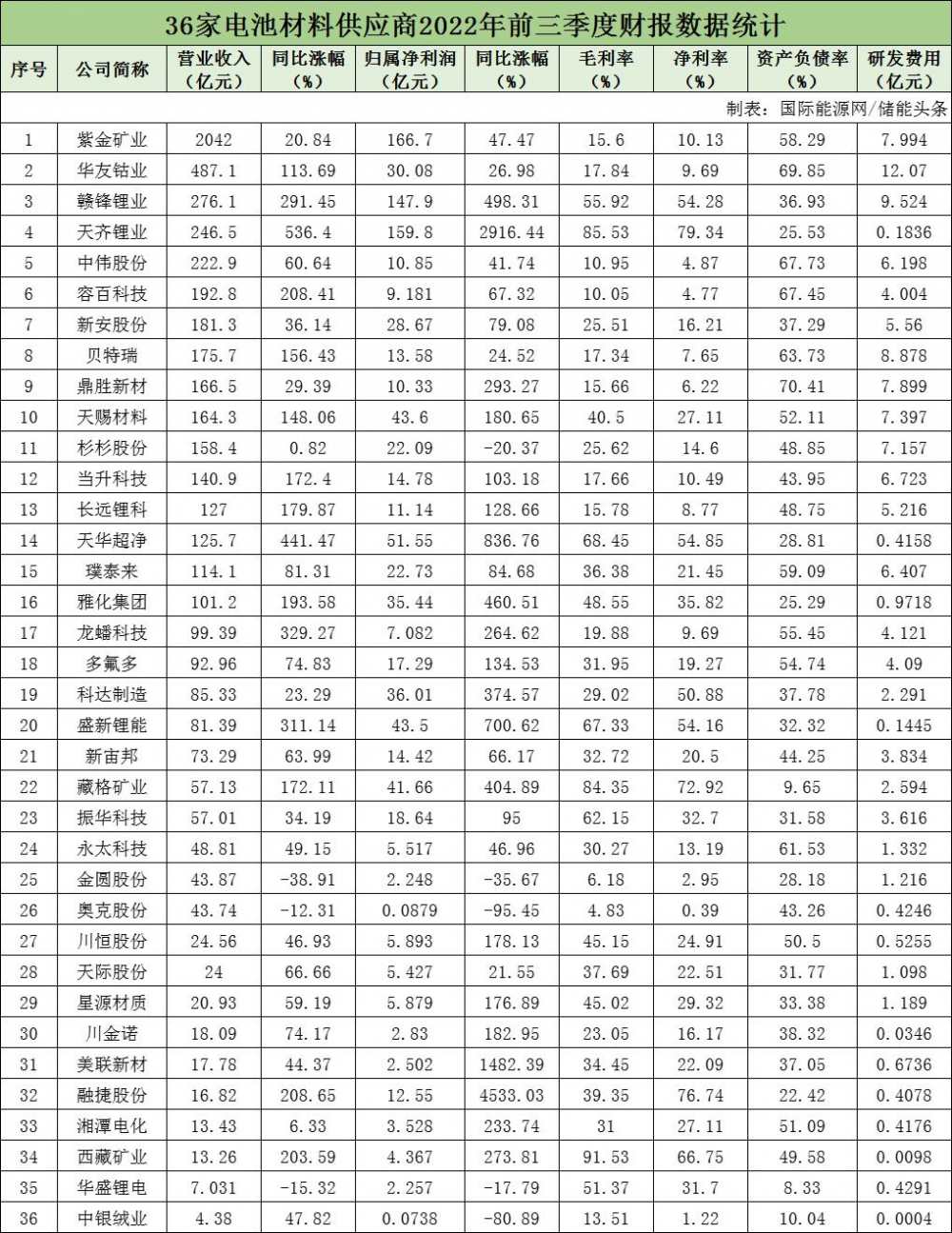

Battery materials enterprises: electrode materials, lithium mining enterprises outstanding performance

In the third quarter of 2022 has released the 36 battery material companies, operating revenue, net profit showed a year-on-year growth trend, even doubled, enterprise performance is quite bright. In terms of the overall liability ratio, most battery material enterprises have a normal level of asset liability, among which the lowest liability ratio of Huasheng lithium battery is 8.33%.

In recent two years, driven by downstream market demand and limited production capacity, the price of upstream battery raw materials continues to rise. Affected by this, lithium electric material enterprise performance is very bright. In the first three quarters, the operating revenue of Rongbai Technology reached 19.28 billion yuan, with a year-on-year growth of 208.41%; Net profit of 918 million yuan, up 67.32% year on year; The company said in the report that its significant growth in the first three quarters was mainly due to strong demand in downstream markets.

The third quarter report showed that the profit of the third quarter of this year was affected by raw material price fluctuations and customer inventory policy adjustment and other accidental factors. Let the relevant person in charge of science and technology, said the li-ion battery material industry chain in the third quarter profit fell, li-ion battery materials affected by raw material inventory write-down and lithium hydroxide spot price procurement is relatively serious, along with the science and technology continuously enrich the product matrix, the layout of the company in the electric field of sodium will significantly enhance their own ability to resist risk, accelerate the anode materials industry leading in the world.

In addition, Shanshan Shares, a leading anode material enterprise, achieved operating revenue of 15.84 billion yuan in the first three quarters, with a year-on-year growth of 0.82%; Net profit attributable to shareholders of listed companies was 2.21 billion yuan, decreasing by 20.36% year-on-year; The non-net profit attributable to shareholders of listed companies was 1.96 billion yuan, up 47.1% year on year.

Third quarter report said the company's core business lithium battery anode material and polarizer business to maintain steady growth. The decline in net profit was mainly due to the decrease in non-recurring profit and loss compared with the same period last year, when the Company completed the transfer of part of the equity of Hunan Shanshan Energy Technology Co., LTD. (now renamed as "BASF Shanshan Battery Materials Co., LTD."), receiving investment income of approximately RMB 1.4 billion.

Since the middle of August this year, the price of lithium salt has broken 500,000 yuan/ton again, and continued to rise, the latest average price has broken 540,000 yuan/ton. With the rise of lithium salt prices, lithium mining companies have been improving performance. Has disclosed the performance forecast of lithium mining company in the third quarter performance continued to rise, a substantial increase year-on-year. Tianqi Lithium and Ganfeng Lithium are still in the lead. Among them, Tianqi Lithium estimates that the net profit of the third quarter is 5 billion yuan to 6.5 billion yuan, with a year-on-year growth of 1026.10%-1363.92%; Ganfeng Lithium estimates that its net profit for the third quarter is 7.046 billion yuan to 8.046 billion yuan, with a year-on-year growth of 567.19% to 661.88%.

According to the disclosure of three quarterly reports and performance forecast of the company, a number of lithium mining companies in the third quarter return to the mother net profit growth. Among them, Ganfeng Lithium is expected to grow by 89%-116% quarter-on-quarter.

Insiders said that the rising trend of lithium salt price in 2022 is confirmed, and the supply and demand pattern from 2023 to 2024 is difficult to reverse. The rising price of lithium salt continues to exceed market expectations, and the performance of lithium mining enterprises in the fourth quarter of this year is still expected to maintain a growth trend.

Energy storage battery enterprises: a number of enterprises profit repair obvious

Since this year, China's new energy vehicle market continues to be hot, directly driving the power battery industry boom degree. First-tier and second-tier listed battery companies such as Ningde Times, Guoxen Hi-tech, Yiwei Lithium Energy and Xinwangda all recorded record single-quarter revenue in the third quarter.

With the transmission of the price mechanism, the profitability of the battery factory began to recover. In the third quarter of Ningde Times, the operating revenue of Ningde Times was 97.369 billion yuan, a year-on-year increase of 232.47%, and the net profit attributable to shareholders of listed companies was 9.423 billion yuan, a year-on-year increase of 188.42%. Set the Ningde era of the highest single - quarter revenue and net profit level. It is understood that the battery shipment of Ningde Times in the third quarter reached 90GWh, of which energy storage battery shipment accounted for about 20%. The company said on its earnings call that energy storage gross margins had returned to double-digit levels in the third quarter, with improved margins on new projects.

The continuous repair of the profitability of Yi Wei Lithium Energy cannot be separated from its active layout of the upstream supply chain. In its financial statement, the company said it has strengthened supply chain management and actively carried out upstream supply chain layout. Continue to promote in-depth strategic cooperation with upstream companies, through the establishment of joint ventures with upstream companies to achieve strategic synergy, on the one hand to ensure the stable supply of raw materials, on the other hand to reduce the procurement cost of raw materials.

In addition, residential energy storage company PI Energy Technology reported a jump in net income and revenue in the third quarter. Thanks to the rapid growth of shipments, the revenue in the first three quarters grew by 6.0%, 27.7% and 65.0%, respectively. In the third quarter, Peineng Technology shipped nearly 1GWh, up 110% year on year and 55% quarter on quarter.

It can be seen that in the first half of the year, the situation of "increasing revenue but not increasing profit" of energy storage battery enterprises due to the rising price of raw materials was reversed in the third quarter, and many enterprises' earnings were obviously repaired. Overseas markets have also become a major driver of growth for energy storage battery companies.

Energy storage PCS enterprise: only 1 enterprise suffered losses

As another important device of current energy storage system, PCS market demand is constantly expanding. In the first three quarters of 2022, 13 of the 14 energy storage converter companies reported positive revenue growth, while only one reported a loss.

Specific enterprises, although the revenue of Huichuan technology is not the Sun power, but the net profit far ahead of other enterprises. The company achieved a revenue of 16.241 billion yuan in the first three quarters, up 21.67% year on year; The net profit of the mother was 3.085 billion yuan, up 23.79% year on year. The change in performance was mainly attributed to the rapid growth of the company's general automation and industrial robot businesses; Thanks to the increasing penetration rate of new energy vehicles and the increasing volume of the company's designated models, the company's new energy vehicle business has achieved rapid growth.

In addition, photovoltaic inverter enterprises are also active participants in the energy storage link. Companies such as Sunshine Power, Jinlang Technology, and De Ye Share also benefited from high shipments, doubling their net profits. As a result of the increase in energy storage business, Suneng Electric also saw a revenue surge in the third quarter, with operating revenue of 645 million yuan in a single quarter, up 156.13% year on year, which was a turnaround from the previous two quarters.

Battery management system companies: Five companies were less profitable than a year ago

As an early warning weapon of energy storage security, BMS has attracted much attention. Storage Semiconductor sorted out six listed battery management system companies, and all six companies made profits in the first three quarters of 2022. It is worth noting that except for Juhua shares, the profitability of the remaining 5 enterprises are lower than the same period last year.

It is understood that the revenue of Juhua Stock in the first three quarters of 2022 is about 16.377 billion yuan; Net profit attributable to shareholders of the listed company was about 1.699 billion yuan, up 557.2 percent year-on-year. The change in results was mainly due to the year-over-year increase in the Company's product prices, raw material prices and energy prices during the current period. The company has strengthened management, ensured safety, improved efficiency, optimized structure, stabilized production, expanded market, seized opportunities, maintained flexibility, pertinency and initiative in production and operation, effectively responded to the increasing downward pressure of COVID-19 prevention and control, the fierce competition in the product market, especially the HFCs market, and the rising costs of raw materials and energy. We achieved safe, stable and high-quality operation of the industrial chain, increased production and sales of major products, increased revenue and profits, and significantly increased the revenue of main businesses over the same period last year. We seized market opportunities, absorbed some of the rising costs of raw materials and energy prices, improved overall operational efficiency, and improved the profitability of main businesses.

In addition, Jiacou became the one with the largest year-on-year revenue decline among the six enterprises. In the first three quarters of 2022, the total revenue reached 412 million yuan, down 20.7% year-on-year. Net profit returned to the mother was 20.93 million yuan, down 71.5% year-on-year. In this regard, Jiatou said on the investor interactive platform that most industries were greatly affected by the epidemic this year. Although the company was affected by the epidemic in order delivery and site construction, the overall order volume in hand had reached 860 million by the disclosure date of the semi-annual report, which increased by 60% compared with the same period last year.

Energy control system enterprise: All revenue achieved positive growth

It is found that the revenue of 8 listed companies with energy control system has all achieved positive growth. Beijing Kerui, China from the first three quarters of the technology loss.

In terms of specific enterprises, Zhongtian Technology achieved revenue of 29.2 billion yuan in the first three quarters, down 20.93% year-on-year; Net profit was 2.47 billion yuan, up 400 percent year-on-year. It is worth noting that the gross profit margin of Zhongtian technology in the third quarter reached 18.19%, a year-on-year increase of 2.25 percentage points, a quarter-on-quarter increase of 2.32 percentage points, a relatively high level in recent years. In this respect, the company explained to the reporter that, because the company made a strategic arrangement this year, the commodity trading business was divested, this part of the business can contribute more than 10 billion yuan in revenue last year, accounting for about 22% of the total revenue, the loss of this part of the business, the revenue will be greatly affected. However, the commodity trading business did not have high gross margins before, and the company's focus on high-end manufacturing with higher value-added technology has been more beneficial to the business.

Guodian Nanrui has the best profitability among energy control system enterprises, with a revenue of 25.616 billion yuan in the first three quarters of 2022, up 10.26% year on year; Net profit attributable to mother was 3.655 billion yuan, up 14.49 percent year on year. In the third quarter of 2022, the company's single-quarter main business revenue was 9.294 billion yuan, up by 10.28% year-on-year; Net profit attributable to mother in the single quarter was 1.545 billion yuan, up 14.53% year on year; The non-net profit of the single quarter was 1.539 billion yuan, up by 16.0% year on year; The debt ratio is 39.38%, the investment income is 17,023,800 yuan, the financial expense is -394,932,400 yuan, the gross profit rate is 28.27%.

Energy storage system companies: 11 companies saw revenue growth

A review of disclosed earnings reports found that of the 17 energy storage system companies, 11 saw their operating revenues rise from last year, while five reported losses.

Among them, although the first three quarters of Shanghai Electric revenue 77.622 billion yuan, but the net profit - 278 million yuan, compared to the same period last year - 3.768 billion yuan significantly reduced the loss. Industry researchers pointed out that the main business of Shanghai Electric is divided into four parts: intelligent energy, intelligent manufacturing, intelligent infrastructure and industrial Internet. The business of thermal power, "landscape hydrogen storage", industrial intelligence and other core tracks has maintained a strong growth trend this year. Driven by multiple factors such as energy supply guarantee + peak demand adjustment + intermittent power shortage in some parts of the country, thermal power investment has reached an inflection point, while new energy and energy storage investment maintains a high business climate, and the company's future orders will continue to grow significantly.

;){kind=link}